Top 100 Financial Institutions

Winds of Change Rattle the Top

Source:cw

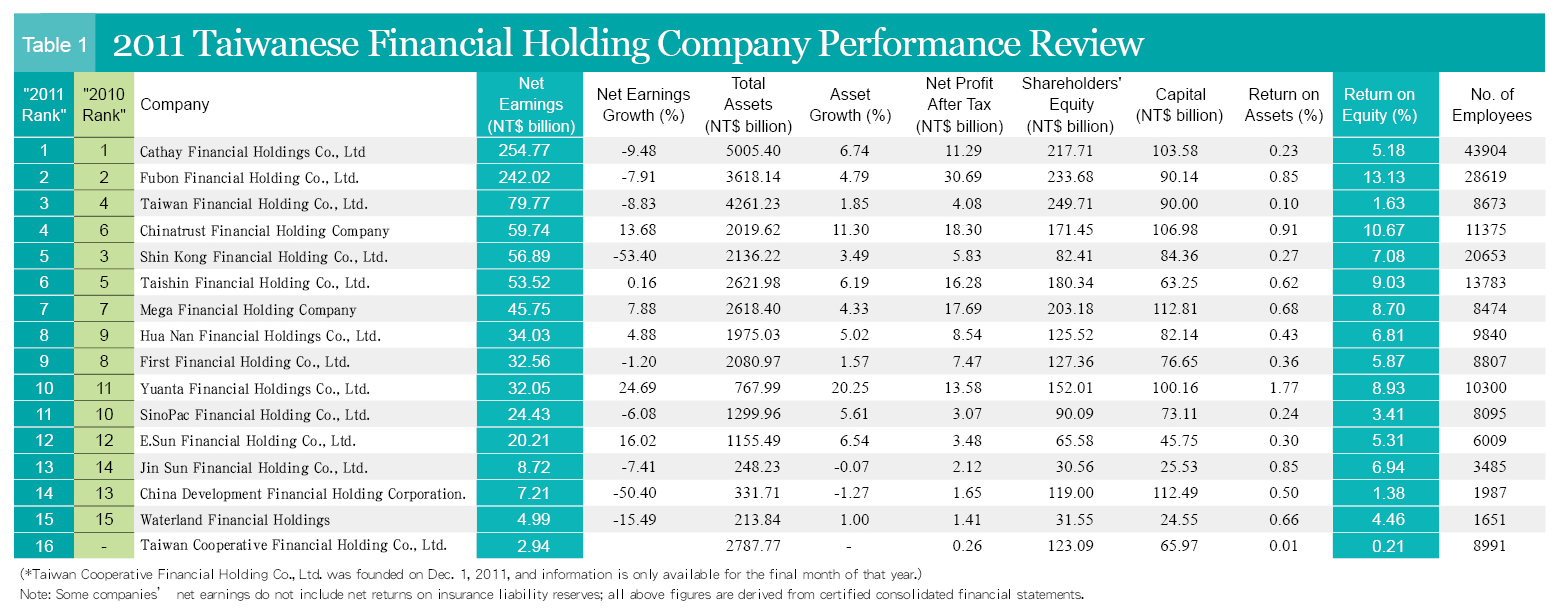

In 2011 Cathay Financial Holdings regained its throne as Taiwan's top financial holdings group, and Bank of Taiwan fell from the Top 10 for the first time, as state-run banks lost their competitive edge.

Views

Winds of Change Rattle the Top

By Judy LinFrom CommonWealth Magazine (vol. 496 )

CommonWealth Magazine's recently-released rankings of Taiwan's 16 financial holdings groups and top 100 financial institutions show that there have been fierce winds of change blowing at the top of the nation's financial heap.

Cathay Financial Holdings total assets topped NT$5 trillion for the first time last year as the group regained the throne it had ceded to Fubon Financial three years ago. Yet Cathay still came up short in terms of operational efficiency as after-tax profit was just one-third that of number-two Fubon. (See Table)

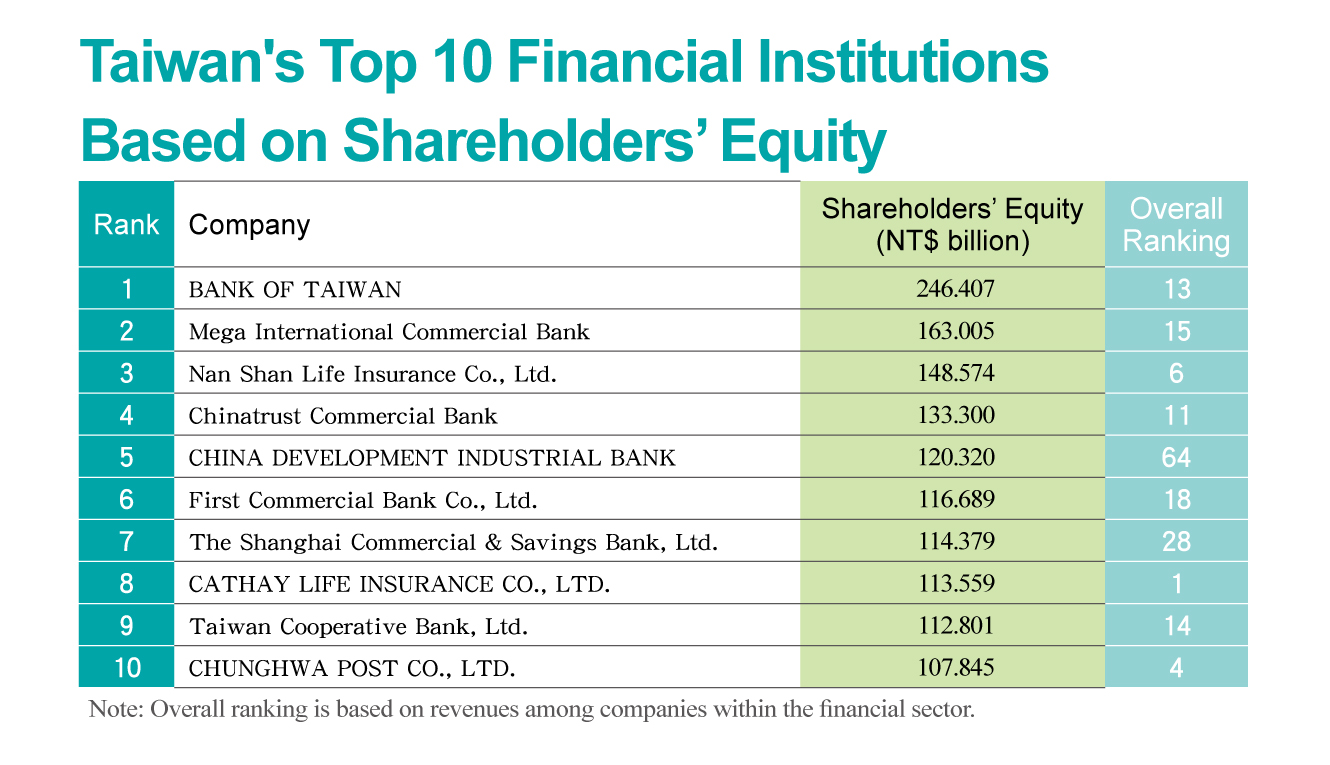

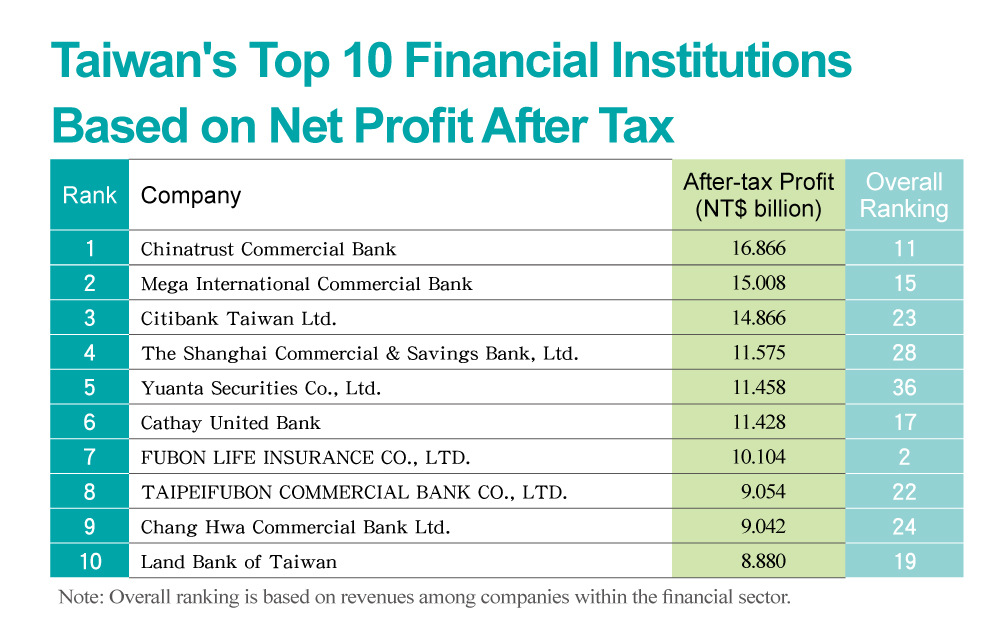

The shifts in the rankings of the top 100 financial institutions were even more startling. Operating revenue at Chinatrust Commercial Bank exceeded that of state-run rival Bank of Taiwan (BoT) for the first time last year, while Chinatrust's after-tax profit of NT$16.8 billion was 4.5 times that of BoT. Private-sector Chinatrust's surge ahead of the nation's biggest state-run bank could safely be described as a watershed moment in Taiwanese banking history.

For the first time ever, BoT was squeezed out of the top 10 in financial institution rankings, and it was the only bank to book negative growth in operating revenue, largely the result of underwriting financing for numerous government policy initiatives and the default of ProMOS Technologies on a syndicated loan led by BoT. Among state-run institutions, those performing relatively well included Taiwan Cooperative Bank, Megabank and First Commercial, all of which not only notched double-digit growth in operating revenue, but also managed to maintain their positional rankings.

While the operating environment in 2011 was tougher for Taiwan's financial sector than the previous year, CommonWealth Magazine's survey of the top 100 financial institutions showed that 63 of them posted growth in operating revenue on the year, compared with just 51 in 2010, and cumulative after-tax profit for the top 100 grew 17 percent, a reasonably impressive performance.

Bond and equity markets were severely rattled in the second half of 2011 as global markets took a beating resulting from the deepening U.S. debt crisis and round two of the European debt debacle, just as financial regulatory agencies across the globe were tightening standards on capital adequacy and other criteria in response to the third of the Basel Accords (Basel III) agreed upon by members of the Basel Committee on Banking Supervision in 2010-2011. But these challenges served Taiwan's financial enterprises with an opportunity to prove their mettle.

Among the most profitable of Taiwanese financial institutions last year, nine of the top 10 were banks, and after-tax profit at the top seven was in excess of NT$10 billion.

As one securities analyst noted, both earnings on interest and processing fees accounted for about half of Chinatrust's total earnings; seldom does a consumer banking business enjoy such a salubrious balance.

"Its leadership in consumer banking will be tough to beat," the analyst says.

Megabank's after-tax profit for 2011 surpassed NT$15 billion, up 35 percent from the previous year and its best performance in the past three years as the bank benefitted from strong growth in its U.S. dollar-denominated lending business.

Moves by China's central bank to exert macro-controls to tighten the money supply resulted in more operating room for overseas branches and provided an opportunity for the relatively more capable overseas banking units (OBUs) of Taiwanese financial institutions to fill the gap in demand for financing from Taiwanese businesses operating in China.

Foreign currency-denominated lending at Megabank, Chinatrust and First Commercial accounted for more than 30 percent of their lending business, as those three institutions capitalized on the fresh wave of financing demand from China-based Taiwanese businesses. The relatively higher interest rate spread on U.S. dollar-denominated lending provided a major boost to profitability at these banks.

Among foreign banks, Citibank maintained its leading position with NT$14.8 billion in after-tax profit and 42-percent profit margin, while the 40-percent profit margin Standard Chartered posted for last year was a massive improvement on its 14-percent profit margin in 2010.

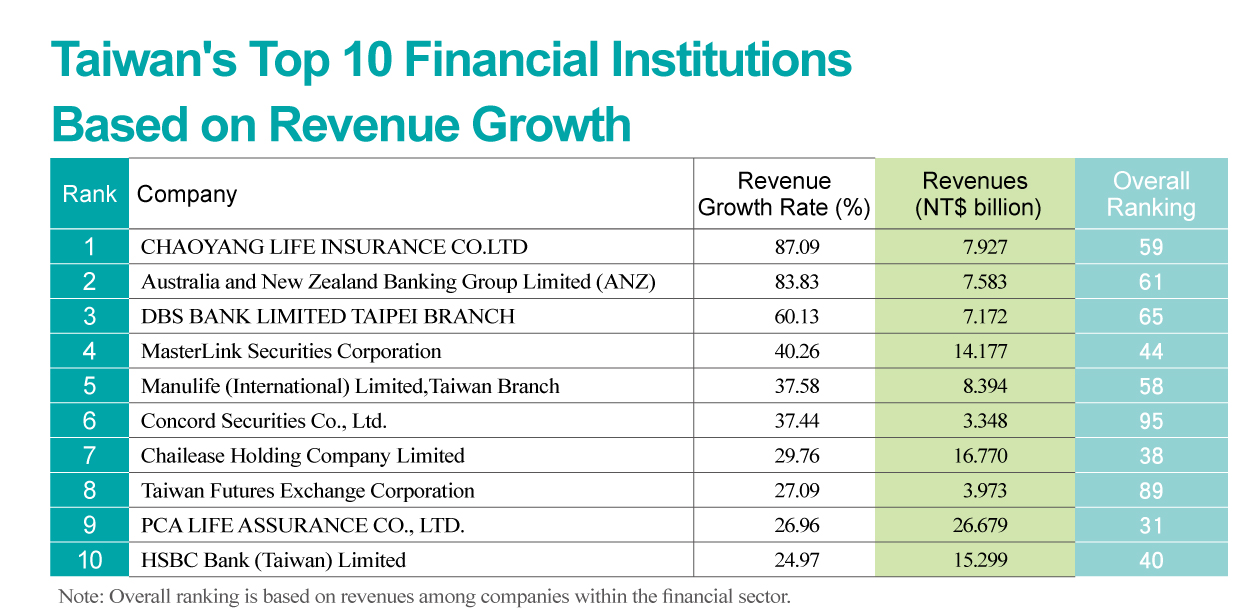

ANZ and Development Bank of Singapore (DBS) posted the highest growth rates in operating revenue, largely due to their focus on consolidation efforts in 2010. Once those efforts were completed last year and their focus returned to expanding their business, the two posted outstanding operating revenue growth rates of 83 percent and 60 percent, respectively.

With the Executive Yuan's Financial Supervisory Commission demanding that banks raise their required reserve and coverage ratios, many banks were forced to increase deposit reserves and shed non-performing loans more aggressively than they had in the past, resulting in a situation where operating revenue outperformed profitability. This also highlighted the advantages of those initially relatively robust banks in operating from a position of strength in a tightening regulatory environment.

In the securities sector, Yuanta Securities maintained its leading position and was the only securities business with profits in excess of NT$10 billion and a profit margin of 61 percent. Yuanta profits were boosted by a cash infusion of NT$8 billion through sales of its shares in Taipei 101 and Maybank Kim Eng Securities in Singapore. Yuanta looks set to comfortably maintain its leading position in Taiwan's securities sector after its parent company last year announced a merger with Polaris' securities, investment trust and futures units, setting the base day for the merger on April 1 of this year.

After the merger with Polaris, Yuanta's service network will expand from 141 to 189 outlets, while its share of the brokerage market will expand from 11 percent to 15 percent. Its share of both the margin trading and securities lending markets will also increase by around five percentage points. Meanwhile, the merger will raise the total value of its warrants issued to 29.02 percent of the market, and the total number of individual warrants issued to 22.95 percent of the market, making it the uncontested leader in both categories.

Additionally, Grand Cathay Securities, a majority-owned unit of China Development Financial Holdings, in early April offered NT$54.6 billion to acquire KGI Securities Co., which will boost its market share of the warrant issuance, brokerage and margin trading business to put it in close running behind Yuanta Polaris and likely vault it into the top spot in equities and bond underwriting.

Owing to an ongoing dispute over the capital gains tax, turnover volume on the Taiwan Stock Exchange has shown a marked contraction this year and it appears that there may be an acceleration of amalgamation among the many local securities firms that once did daily battle in the heyday of Taiwan's securities markets.

"This year may be the first year of amalgamation, but next year it will become a year of elimination," one analyst predicted.

Market laws of survival of the fittest may force smaller, less competitive securities firms into a downward spiral of losses and, consequently may potentially accelerate the process of amalgamation among securities firms.

Hedge Capability Determines Life Insurers' Fortunes

In the insurance sector, Cathay Life unsurprisingly remains at the top of the heap, but Fubon Life's profits in excess of NT$10 billion do catch the eye.

Fubon Financial president Victor Kung told a shareholders' meeting that the company's efforts at controlling hedging costs had borne outstanding results and boosted overall profitability.

Another factor playing a role in the company's profitability was the outstanding returns gained from investments in Taiwanese equities.

As one insurance company executive put it, the life insurance market has now shifted from its former "sales war" to a "financial war." Older companies such as Cathay and Shin Kong are burdened with long term negative interest rate spreads and must continually develop new products to find equilibrium. Thus, whoever is able to reduce hedging costs to the lowest level possible through financial management will see that reflected on the bottom line of their financial reports.

With China and Taiwan set to ink a "Cross-Strait Investment Protection Agreement," all eyes are now focused on the establishment of a renminbi account settlement mechanism that would allow Taiwanese financial institutions to engage in renminbi-denominated business.

There are none in the Taiwanese financial sector who are not licking their chops at the prospect, not only drawing up plans for expansion into the China market, but also exploring strategic alliances with Chinese financial institutions, to add teeth to those expansion plans.

As Taiwan's entire financial sector sees it, 2012 represents a year of both opportunity and challenge. While there has been a turn for the better in terms of official government policy and market deregulation, sweeping changes in the greater market environment also mean there will be a drive to rethink those market sectors in which financial institutions will seek to compete. It should be an interesting spectacle as this grand business drama of our age plays out among financial institutions.

Translated from the Chinese by Brian Kennedy

Views

Subscribe to CWE Newsletter (every Thursday)

Stay abreast of what's happening in Taiwan with our weekly digest.