Loosening Currency, Raising Wages

China Shoots for Soft Landing

Source:cw

Over the past two or three months, China has quietly adopted some seemingly contradictory policy measures "a soft landing amidst shaky conditions" and a smooth transition as the reins of leadership change hands.

Views

China Shoots for Soft Landing

By Shu-ren KooFrom CommonWealth Magazine (vol. 489 )

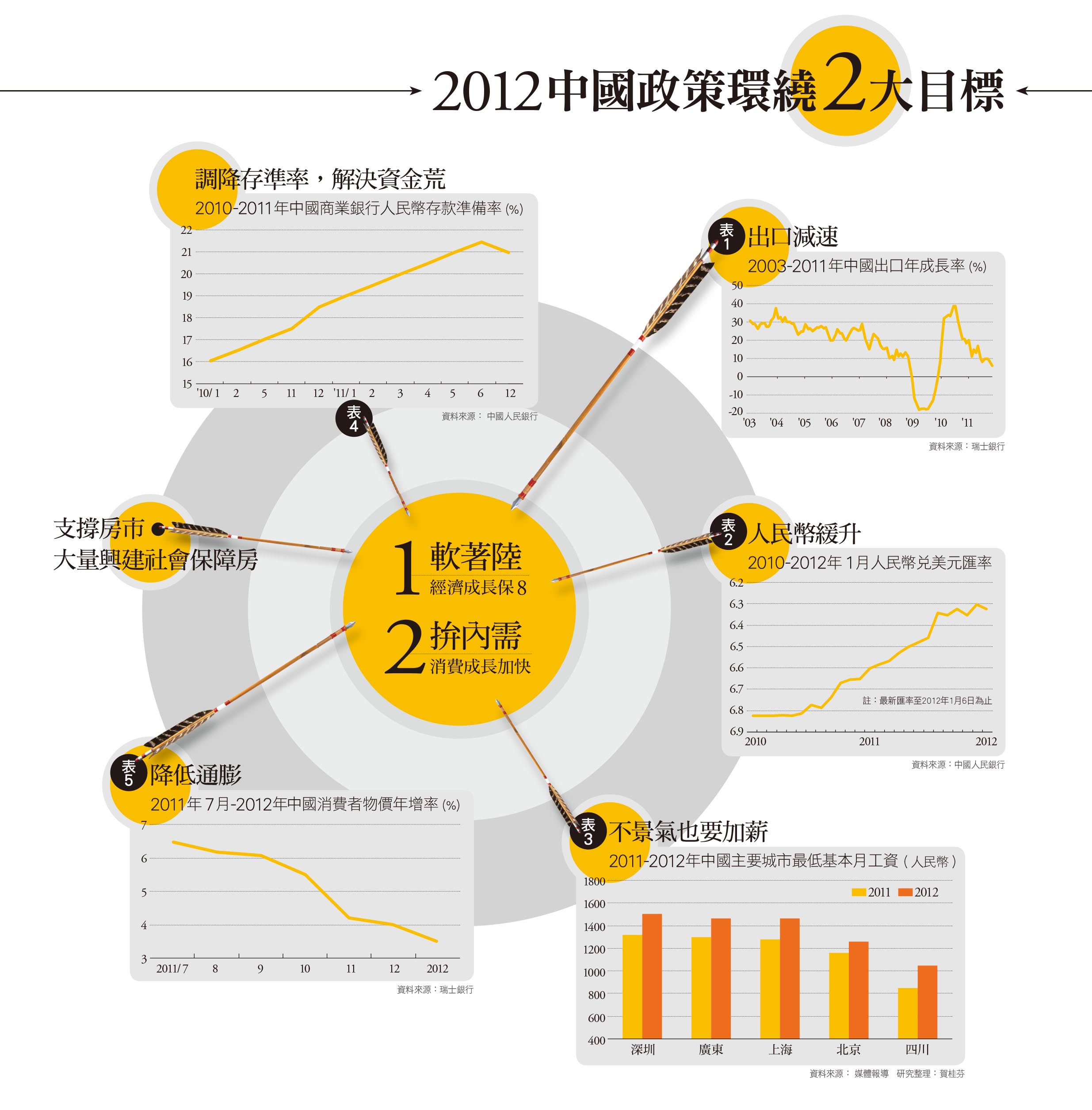

There is by now broad market agreement that China will see softening economic growth in 2012. The just-concluded session of China's Central Economic Working Conference set the tone for this year's economy as "advancement amidst stability."

With the European debt crisis yet unresolved, external demand remains weak and the National Bureau of Statistics of China has announced that its purchasing managers' index (PMI) dropped below 50 for November of last year, the first time the manufacturing sector has slid toward a contraction in nearly 30 months.

The Organization for Economic Cooperation and Development's (OECD) index of leading indicators, as well as China business confidence indices arious other organizations , all point to a slowing of China's economic growth beginning in the fourth quarter of 2011.

Everyone from Chinese officials and international organizations down through various major financial institutions are now routinely forecasting that economic growth for 2012 will slow to eight percent, down from nine percent the previous year.

While that remains far higher than most other countries, given the 10 percent average annual clip China has grown at during the last three decades, those two percentage points may well be enough to result in mass unemployment, and the potential for social unrest that could entail.

The key period as to whether China's economy can make a soft landing will be the first quarter of 2012. During a recent tour of Hunan Province, Premier Wen Jiabao candidly stated: "The first quarter may get tougher."

Consequently, over the last two or three months, China's government has pushed forward a succession of currency, taxation and property market policy initiatives in an all- out effort to prop up domestic demand, particularly in the property and consumer markets, and avert an economic hard landing.

Weak overseas demand is the chief culprit behind China's economic slowdown.

The looming debt crisis in the European Union, its largest export market, began to put the brakes on China's export growth rate two months ago. Some financial institutions are even forecasting that exports may contract in the first quarter of this year, perhaps stalling export growth figures for the entire year.

Although exports account for only about 15-20 percent of China's overall economic growth, they account for 40 percent of growth in manufacturing sector production value,and any decline in exports would be a major blow to the manufacturing sector.

Market Revival Policy 1: Gentle RMB Appreciation

Weak exports may prompt the People's Bank of China (China's central bank) to consider decelerating the pace of appreciation in the renminbi exchange rate, a mechanism having a profound impact on the profitability of export-oriented businesses.

Even if the central bank's fundamental approach to foreign exchange policy remains unchanged, with the European debt crisis looming, global investors are recalling capital back from China and emerging markets and returning it to dollar-denominated assets to hedge against risk, resulting in an outflow of capital from China and putting depreciatory pressure on the Chinese currency.

At the end of last year, the renminbi's exchange rate against the U.S. dollar stood at 6.35 to 1, a cumulative appreciation of 3.65 percent on the year. Swiss bank UBS has forecast that the exchange rate at the close of this year will stand at RMB 6.15 to 1, a slight downtick in the annual pace of appreciation to three percent.

After Premier Wen Jiabao's public directive last October that "farsighted micro-adjustments must be made to government policies whenever appropriate and to whatever appropriate degree," banks were instructed to increase lending to smaller private companies and reduce their interest rates on that lending.

A little over a month later, People's Bank of China monetary policy took an abrupt turn.

With inflationary pressure easing, China's central bank for the first time in three years lowered the required reserve ratio for commercial banks, by a half a percentage point, freeing up an estimated 400 billion renminbi for the money markets.

The market is widely anticipating that the bank will lower the required reserve ratio once again in January in an effort to resolve the credit crunch issue among SMEs.

Qu Hongbin, lead economist for HSBC, believes growth has supplanted controlling inflation to become the core consideration driving policy decisions and expects the coming months to see increased official enthusiasm for looser policies and easing of lending limits in the coming year.

Market Revival Policy 4: Official Action on Property Market

In the property market, the biggest single influence on Chinese domestic consumption, things seem less than upbeat following indications from officials in top- tier cities like Beijing, Shanghai, Guangzhou and Shenzhen that market control measures mostly amounting to purchasing limits would continue in the coming year.

According to UBS forecasts, the floor space of commercialhousing sales and new construction start-ups will decline about 10 percent on the year and that will act as a drag upon the steel, automotive, home appliance and other domestic demand industries that construction activity and investment indirectly influence.

But China's Ministry of Housing and Urban-Rural Development already has plans for construction to begin on seven million public housing units public housing units this year. Although that figure is 20-30 percent off from last year, with the addition of the work and investment involved in other, already planned, public housing units set to enter their actual construction phase this year, it should be enough to offset any weakness in the commercial housing market.

Led by the public housing market, overall urban and rural real estate floor space under construction this year is forecast to achieve a 10- percent growth rate in 2012. Overall property market investment is expected to grow between 15 and -20 percent.

UBS economist Wang Tao believes that even though growth will be 10 percentage points below that of last year, this will be enough to prevent a hard landing for the property market and the overall economy as well.

China's economy has suffered through two hard landings in recent decades, once in the fourth quarter of 1999 in the wake of the Asian financial crisis and another, more serious, episode in the first quarter of 2009 following the global financial meltdown. In both cases the economic growth rate was below seven percent, and both were the result of external factors.

Given that perspective, Dr. Ho-Mou Wu, a professor of economics and executive vice president at Beijing University's National School of Development, believes that unless the European debt crisis spirals completely out of control, China's economy should be able to maintain growth at eight percent or higher, and that should be enough to forestall any hard landing.

Additional research by Jin Chen

Translated from the Chinese by Brian Kennedy

Views

Subscribe to CWE Newsletter (every Thursday)

Stay abreast of what's happening in Taiwan with our weekly digest.