Big Companies, Low Taxes

The Secrets behind the Shortfall

Source:CW

Taiwan's government is desperate for revenues, but the country's corporations pay lower tax rates than salaried workers. Many use the same overseas tax dodges that Apple made famous, and lawmakers are helping them get away with it.

Views

The Secrets behind the Shortfall

By David Huang, Yi-Shan Chen, Uidy KaoFrom CommonWealth Magazine (vol. 523 )

May 3 was a normal Friday, seemingly just like any other. But away from the glare of Taiwan's pervasive media, without any debate, conglomerates, Taiwanese businesses operating overseas and majority Kuomintang legislators teamed up to block an amendment to Taiwan's Income Tax Act that would prevent companies from avoiding taxes by booking and keeping their profits overseas.

The revision, which had already cleared its first reading in the Legislative Yuan (a bill has to clear three readings to become law), was removed from the body's agenda and sent for consultations between majority and minority lawmakers, to take place out of the public eye.

At a time when the chief executives of multinationals Apple and Google were called to testify on their overseas tax avoidance schemes before the United States Senate and British Parliament, respectively, Taiwan's lawmakers were abdicating their responsibilities, standing in the way of legislation that would allow the government to tax overseas income.

Taiwan has lagged years behind advanced countries and regional rivals on the issue, but it was hoping to finally join the international fight against corporate tax avoidance with this so-called "overseas tax collection provision."

"This is an international tax collection war. Without legislation, we have no weapons with which to fight the war, and we don't even have the right to advocate imposing taxes," says Ulyos K.J. Maa, a senior partner at accounting and auditing firm KPMG Taiwan.

Because Taiwan has no legal basis for taxing overseas income and policy makers have fallen for trickle-down economics over the past 20 years, repeatedly lowering tax rates to stimulate the economy, Taiwan's tax revenues as a percentage of GDP are among the lowest of any country in the world. Taiwan's government also ranks as one of the poorest in the world.

Government Poorer than China, South Korea

Taiwan's tax-to-GDP ratio has fallen from a healthy 20 percent in the 1990s to 12.8 percent in 2011, the seventh-lowest in the world among 60 countries analyzed in Lausanne-based IMD's World Competitiveness Yearbook.

Taiwan's ratio is not only lower than that of the United States, Japan, Hong Kong and Singapore, it also falls well below South Korea's 25.9 percent and China's 19 percent.

Because of the lagging tax revenues, Taiwan has consistently run budget deficits over the past two decades, leaving the government unable to aggressively improve the country's public infrastructure. The result has been a vicious cycle of perpetual economic doldrums.

A former finance minister who participated in Taiwan's meteoric economic rise in the 1970s and 1980s, helping it emerge as the leader of the Four Little Dragons of East Asia (Taiwan, Hong Kong, Singapore and South Korea), laments the country's lack of progress in recent years.

"When you go to China to see what's going on, it changes every three months. Come back to Taiwan, and you realize it hasn't changed for 20 years," he says.

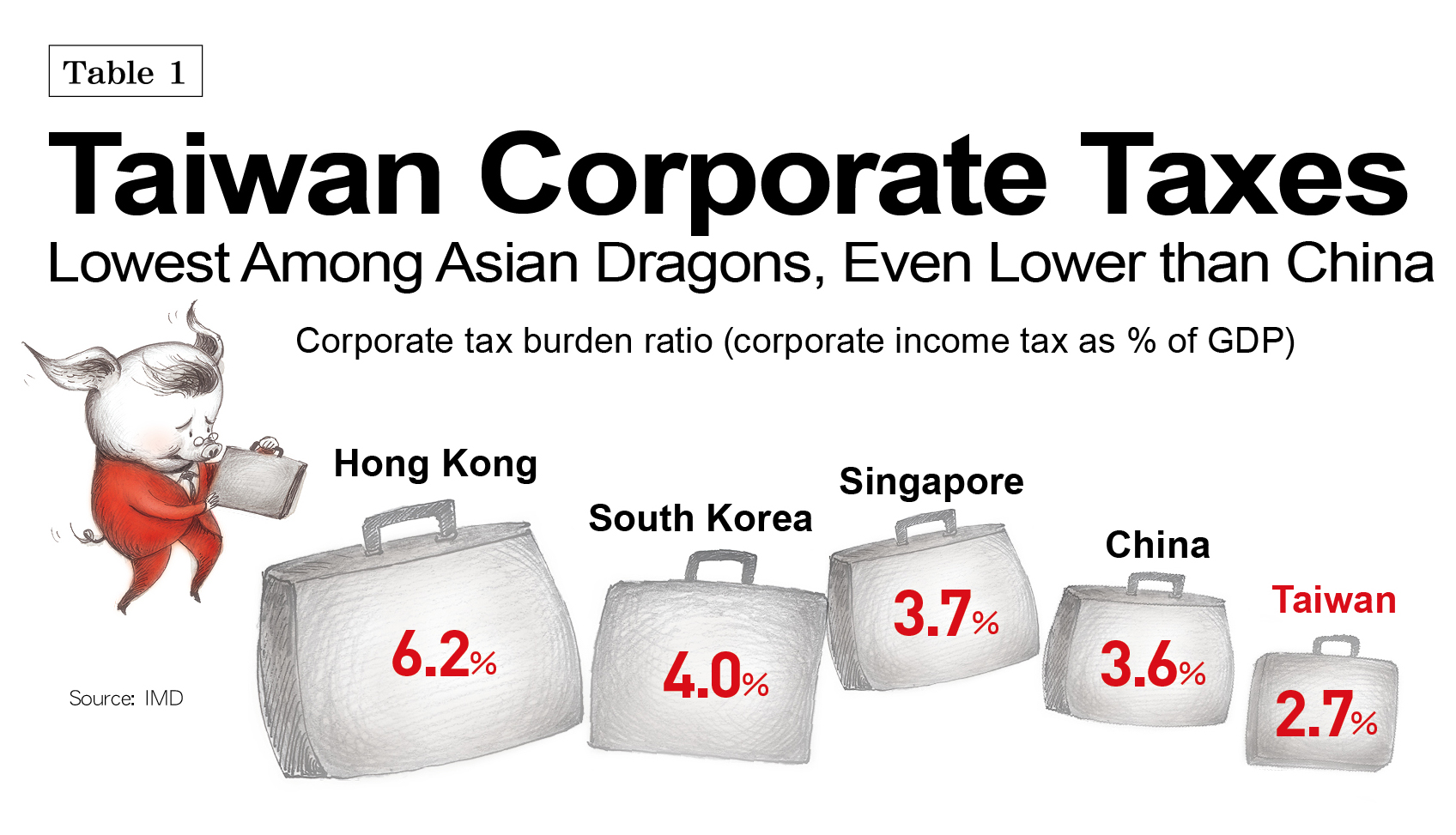

So why is Taiwan's government so poor and why are tax revenues so low? Aside from having already become a low-tax paradise for wealthy individuals, Taiwan is now also a low-tax heaven for corporations. Though leading businessmen regularly take to the media to urge the government to cut taxes, Taiwan's corporate tax rates are, in fact, already low. The overall tax burden of domestic companies is not only the lowest of the Four Dragons, at 2.7 percent of GDP, it is also below China's 3.6 percent and not even half of Hong Kong's. (Table 1)

After taking a closer look at the numbers, CommonWealth Magazine discovered that the bigger the enterprise, the lower the actual tax rate it pays.

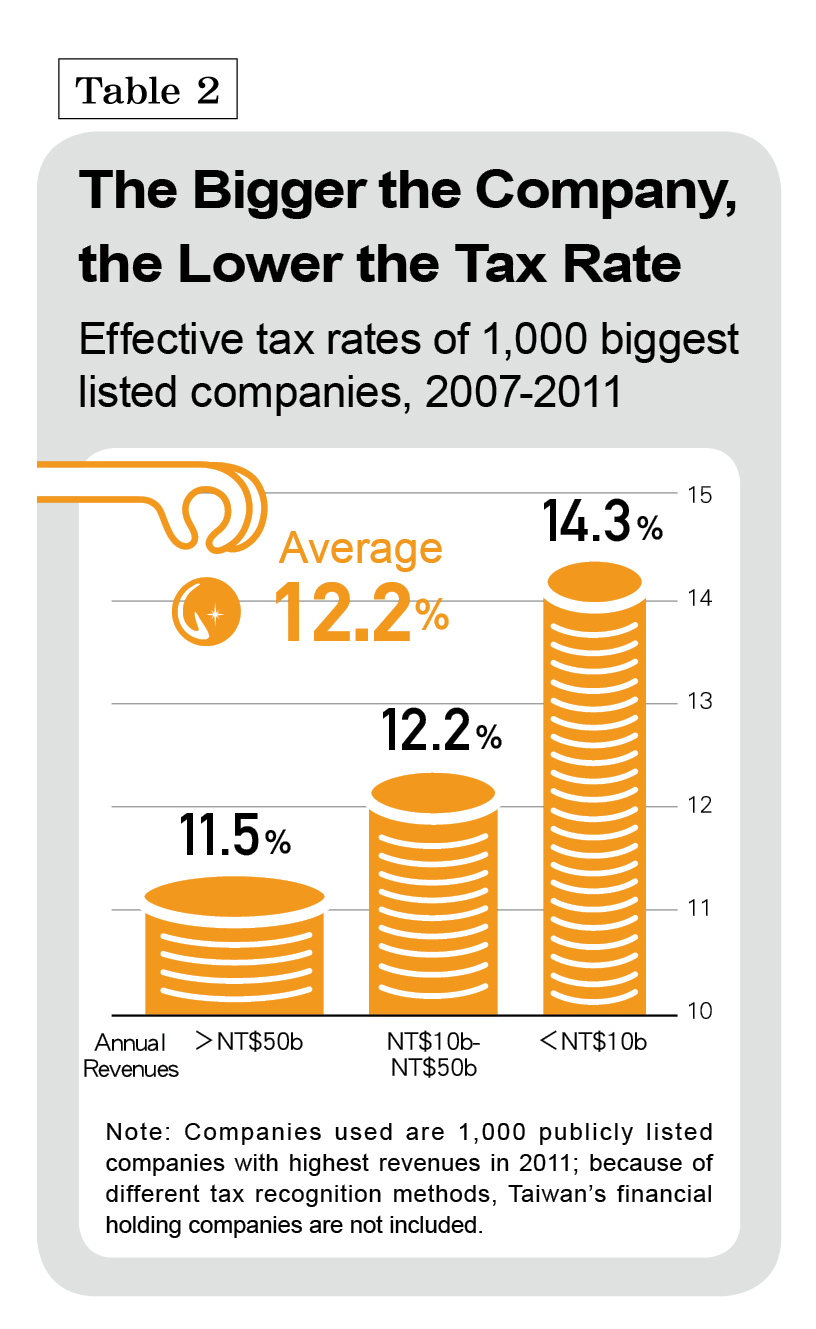

Taiwan's corporate tax rate was lowered to 17 percent from 25 percent in 2009, but for bigger companies, it may not have mattered. A survey by CommonWealth Magazine of the 1,000 publicly listed companies with the highest revenues found that they averaged an "effective" tax rate (total tax paid divided by total earnings) of 12.2 percent on income generated between 2007 and 2011. That's close to the 12 percent marginal income tax rate imposed on middle-class households with annual taxable incomes of between NT$500,000 and NT$1.13 million. (Table 2)

Lower Tax Rate than Wage Earners

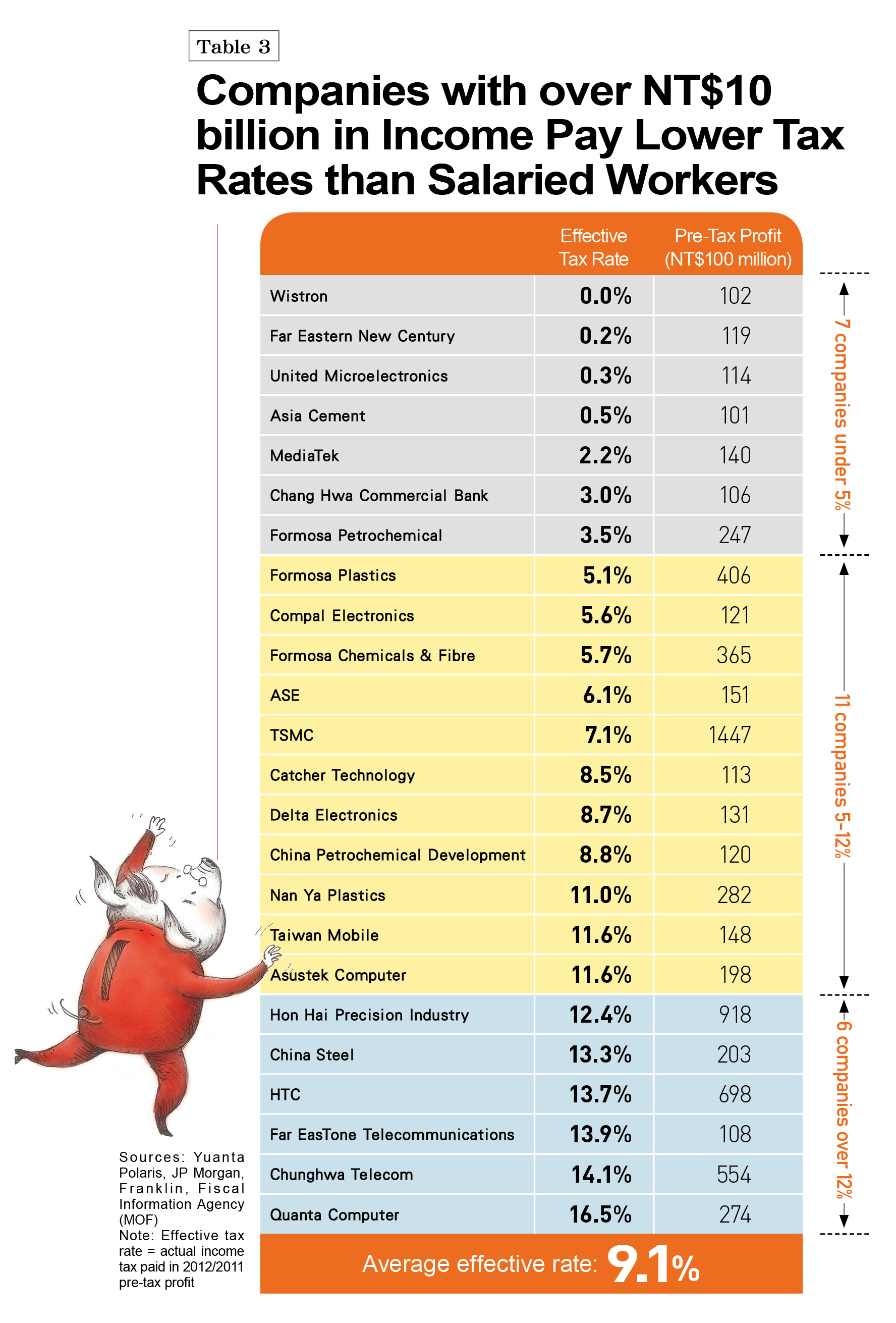

In 2011, there were 24 listed companies with earnings exceeding NT$10 billion. The effective tax rate paid by these high-income earners averaged a mere 9.1 percent, lower than that faced by the average white collar worker. (Table 3)

Indeed, seven of those companies paid effective tax rates of below 5 percent, or lower than the 5 percent marginal tax rate imposed on individual taxpayers in the lowest tax bracket (taxable income below NT$500,000).

Because the National Tax Administration does not release the returns of individual companies, CommonWealth based its calculations on the companies' audited annual financial statements, taking the "income tax paid" figure and dividing it by their pre-tax income to get their effective tax rate.

The companies with effective tax rates below 5 percent on their 2011 income were: Wistron Corp. (no tax paid); Far Eastern New Century Corp. (0.2 percent); United Microelectronics Corp. (0.3 percent); Asia Cement Corp. (0.5 percent); MediaTek Inc. (2.2 percent); and Formosa Petrochemical Corp. (3.5 percent).

IT service provider Wistron did not have to pay income taxes because of a number of exemptions and tax credits. Gains of NT$500 million on a domestic investment and unrealized gains of NT$4.2 billion on overseas investments were tax exempt; Wistron booked a NT$1.6 billion investment loss when one of the companies it invested in reduced its capital to offset losses; and it also benefited from received R&D tax credits.

Albert Hsueh, chairman of PricewaterhouseCoopers Taiwan, recognized CommonWealth's effort, noting that the method used to calculate the effective tax rates was the best when no other alternatives were available. "But it is really surprising that effective tax rates for corporations are so low," he said.

In Taiwan, gains on investments are tax exempt, companies do not have to pay taxes on gains from the sale of land or equities, and the government is powerless to collect taxes on gains from overseas investments, three major reasons why domestic Taiwanese companies pay so little in taxes.

In particular, the migration of assets and profits overseas exposes loopholes in the government's tax collection efforts.

Overseas Investments: The New Tax Loophole

Swept up in the globalization wave, Taiwanese companies began relocating their operations overseas and investing abroad as early as the 1980s, but the country's tax code has yet to catch up with the trend.

Companies with presences overseas have used three major schemes to avoid paying taxes, causing Taiwan's tax revenue reservoir to leak incessantly and leave the country's Treasury starved of funds:

1. Using accounting gimmicks: Seen now as one of the most popular tax avoidance schemes used by multinationals around the globe, "transfer pricing" inflates the profits of overseas subsidiaries of Taiwanese companies while keeping earnings low at home. The result: the profits stay in low-tax havens.

2. Holding funds abroad: Profits made by companies overseas stay there and are not remitted back to Taiwan, keeping them away from local tax collectors.

3. Becoming a foreign entity: Some Taiwanese companies have decided to become foreign entities, turning individual shareholders into shareholders of foreign companies.

Loophole No. 1: Accounting Gimmicks

In the 1980s, large numbers of Taiwanese garment and shoe manufacturers relocated abroad, investing in new factories in Southeast Asia and China. The parent companies in Taiwan helped the overseas subsidiaries process orders and borrow money to fund their growth. Many of these companies then adopted "transfer pricing," allowing affiliates in low-tax havens to retain most of the profits and limiting the earnings booked in Taiwan. As a result, almost no taxes were paid at home.

In 2004, the Ministry of Finance announced auditing guidelines related to "transfer pricing," opening the doors for tax agents to go after untaxed profits overseas. But tax laws remained incomplete, making it impossible to tax overseas earnings that were not remitted back to Taiwan.

Today, Taiwan is already 25 years behind Germany and even six years behind China in cracking down on "transfer pricing" abuses.

Loophole No. 2: Holding Funds Abroad

The second major loophole costing the government tax revenues is the common practice by corporations of holding funds abroad rather than sending them home. And Taiwan's government makes this one easy. According to the country's outmoded tax code, gains on overseas investments are not taxed if they are not remitted back to Taiwan.

China stands out as one of the places where Taiwanese companies stay out of the reach of tax collectors at home. In the 20 years since Taiwan first permitted domestic businesses to operate in China in 1992, Taiwanese enterprises have invested US$126 billion (roughly NT$3.7 trillion) there. If investments around the rest of the globe are added, Taiwanese enterprises have injected US$200 billion into foreign countries during the period, equal to roughly half of Taiwan's annual GDP.

As of the end of last year, 1,198 publicly listed Taiwanese companies had investments in China. Of them 630 reported profits on those investments, but 469 did not remit the profits home, avoiding any tax liability in Taiwan.

Tainan-based Uni-President Enterprises Corp., now a powerhouse in China's beverage and instant noodle markets, originally invested NT$17 billion in the mainland market. Investment gains and cash dividends have increased the book value of that investment to NT$57.9 billion as of the end of 2012, but not a penny of the NT$40.9 billion in accumulated profits has returned to Taiwan, and therefore, not a penny of it has been taxed here.

Last year, Uni-President's effective tax rate in Taiwan was merely 0.93 percent. Among other companies taking advantage of the same loophole, Advanced Semiconductor Engineering Inc. and Compal Electronics Inc. paid only 6.1 percent and 5.6 percent of their pre-tax income in taxes, respectively.

On many listed companies' financial statements, there is one line item in particular that shines light on the loophole: deferred income tax liabilities. Companies with deferred income tax liabilities are essentially saying, "I admit that these are taxes that should be paid to the country, but I'm not paying them right now."

If the National Tax Administration does not keep a tight watch, these potential tax revenues can easily vanish into thin air. All it takes is for companies to decide to keep their sizable overseas profits abroad forever, creating permanent foreign investments that frustrate Taiwan's taxmen.

In 2009, a tax agent at the National Taxation Bureau of the Northern Area surnamed Chen came up against this formidable tax dodge. He noticed that the deferred income tax liabilities of a company registered in the British Virgin Islands, a notorious tax haven, had suddenly fallen to zero. All it took was for the board to resolve that the funds would never be remitted home, and the liabilities legally disappeared from the company's accounts.

But Chen would not let the case go and identified flaws in the company's accounting practices. Because the company did in fact make money, he required it to pay taxes based on the "substance-over-form" tax doctrine, which says that if there are profits, they should be taxed. A Finance Ministry official overruled Chen's decision to tax the company, however, arguing that it had "no legal basis," leaving the dedicated tax agent outraged.

"Taiwan's current approach to taxing overseas investment gains is based on cash-basis accounting. The overseas company has to distribute profits and those gains have to be remitted back to Taiwan before they can be taxed. That creates huge problems," says Dennis Lee, a certified public accountant with Baker & McKenzie, Taipei.

The government is now trying to do something about this. After CommonWealth Magazine highlighted the problem of offshore tax shelters in a story published in September 2012 on Taiwan becoming a low-tax haven for the wealthy, the Ministry of Finance proposed the "overseas tax collection provision" mentioned above.

The amendment to the Income Tax Act would establish "controlled foreign corporation" (CFC) and "place of effective management" rules in line with international practices on preventing tax avoidance. The Cabinet approved the revision in December and sent it to the Legislature for final passage.

The amendment would empower tax authorities to tax profits that are simply reported by companies as "overseas income," without the need for the funds to return home.

Finance Minister Chang Sheng-ford said the ministry consulted the rules set by Western countries such as the United Kingdom, Germany, France and the United States and neighboring countries such as Japan, South Korea and China in establishing the CFC tax system, and he hoped that it would promote tax fairness.

But despite being long overdue and respecting international practices, the amendment has run into stiff opposition from conglomerates and overseas Taiwanese businesses. They have joined with majority Kuomintang lawmakers to put pressure on the Finance Ministry and postpone the legislation's passage.

KMT Legislator Lin Te-fu, a member of the Finance Committee, admitted, "There is a lot of resistance from Taiwanese businessmen operating overseas. It's really intense." Lin is now strongly advocating rethinking the wisdom of amending the law.

Even when faced with the basic necessity of returning profits home to distribute dividends, Taiwanese companies are still obsessed with keeping their money out of the government's hands.

Taiwan Cooperative Bank executive vice president David Fan says many major corporations in Taiwan take out short-term loans to pay dividends simply to avoid facing a tax liability on the funds returned.

"Although companies have to pay interest on the loans, they can claim it as a tax deductible expense," says Cosmos Bank president Richard Chang, pointing to another way corporations avoid paying taxes.

Loophole No. 3: Becoming a Foreign Entity

Amazingly, while financial and taxation agencies were promoting an amendment to crack down on tax avoidance by keeping funds offshore, other agencies have already unwittingly opened the door wider to tax avoidance schemes that cost Taiwan precious revenues.

By allowing Taiwanese companies to turn themselves into foreign entities and then list on Taiwan's stock markets, local authorities have gifted corporations another way to lower or eliminate their tax burden.

In 2008, the government began allowing companies not registered in Taiwan to list and raise funds on the country's equity markets. Their shares were even given the special designation "F shares," with the "F" denoting "foreign."

Many domestic companies underwent quick metamorphoses and turned themselves into foreign entities. Their owners were suddenly treated for tax purposes as shareholders in the newly created foreign entities, entitling them to the more favorable individual income tax rate of 20 percent applied to overseas income.

One obvious example of a corporation engineering such a transformation is Gourmet Master Co., operator of the 85°C chain.

In China, the chain pitches itself as a Taiwanese bakery and café, and it has expanded aggressively. But technically, Gourmet Master is a "foreign company" registered in the Cayman Islands, another notorious tax avoidance paradise.

Cayman Island Registration = Tax Savings

In 2010, Gourmet Master listed on the Taiwan stock exchange as a "foreign company." Its chairman Wu Cheng-hsueh emerged as the board chairman and principal shareholder of a Cayman Islands company.

This transformation enabled Wu and other major shareholders to pay a 20 percent marginal tax rate on the dividends they receive instead of the top marginal tax rate of 40 percent they would have had to pay as shareholders in a Taiwanese company. Wu probably received around NT$80 million in dividends for the 2011 fiscal year based on the 20 million shares he currently holds, which means his status as a shareholder of a foreign company cost national coffers more than NT$10 million in tax revenues.

Corporations can similarly reduce their tax burden significantly by becoming an overseas entity and also steer clear of future tax liabilities in Taiwan.

Jason C. Hsu, a certified public accountant with PricewaterhouseCoopers Taiwan, explains that in the past when Taiwanese parent companies invested abroad, even if their overseas profits could not be taxed unless they were remitted home, Taiwan still retained the power to assess taxes.

"But once the parent company has established itself as a foreign entity, Taiwan's power to tax is gone, and those profits will never return to Taiwan," Hsu said.

In the case of Gourmet Master and its pre-tax profit of NT$1.4 billion, China accounted for about 70 percent of that, or NT$980 million. If that were fully reported by a parent company in Taiwan and remitted back home, tax agencies could collect NT$167 million in corporate income taxes. But with Gourmet Master registered in the Cayman Islands, the profit will remain in the low-tax haven, and Taiwan is now powerless to tax the company's overseas profits.

Jacky M. Chen, a board member of Deloitte and Touche in Taiwan who certifies Gourmet Master's accounts, defended the company's registration in the Cayman Islands. Chen says the company's motivation in making the move was not to position itself to return to Taiwan for its primary listing, because when it was first planning the change in 2007, Taiwan had not yet allowed F shares in its equity markets. Gourmet Master's original plan, Chen says, was to list shares in Hong Kong and attract international capital, which is why it ultimately decided to set up an overseas holding company.

F Shares: Bad Tax Policy by 'Stupid Government'

One certified public accountant who often attends meetings on cross-border taxation and has observed the changing face of Taiwanese enterprises believes companies are not to blame for the trend. Unable to contain his anger, the CPA said the F shares, which turned "rooted Taiwanese companies" into "rootless Taiwanese businesses," were "the product of a stupid government. This is the most typical example of the erosion of a tax base."

Before the creation of F shares, most domestic companies decided to invest overseas in the name of the Taiwanese parent company because of fundraising and talent recruiting considerations, the CPA explained. Now, however, more companies are registering overseas and then coming back to Taiwan to list on domestic equity markets – and they are still absorbing Taiwanese capital and talent.

This CPA managed to calmly explain the growing international trend toward recovering taxes from offshore companies, but when he got started on F shares, his frustration boiled over.

Slamming the table with his hand, he fumed, "These big shareholders were not doing this before. But the F shares were essentially the government teaching them how to take their companies and profits abroad, giving them a convenient opening. Their tax burdens were lowered, and it was all perfectly legal. It's really too much!"

Gourmet Master is just one of many companies that have established themselves as a foreign entity and then returned to Taiwan to raise funds by listing on the Taiwan stock exchange.

From 2008, when then Taiwan Stock Exchange Corp. chairman Schive Chi promoted the idea with the support of former finance minister Lee Sush-der, to today, a total of 50 companies have listed F shares.

Yuanta Polaris Securities executive vice president Randy Ming Jen Yu says F shares were originally intended to attract "rootless Taiwanese companies" to go public back home and then eventually invest in Taiwan. But as the scope of the policy expanded, it ended up enabling "rooted" companies to become "rootless" and then return home to list their shares and raise funds.

Finance Minister Chang Sheng-ford also wants to plug this loophole, and he proposed an amendment introducing "place of effective management" rules that would have made it possible to decide tax residency status based on where the company actually operates rather than where it is registered. That proposal was also blocked by legislators.

Official Disbelief at Low Effective Rates

In recent years especially, Taiwanese officials have bought into the myth that cutting taxes can actually lead to increased tax revenues by stimulating economic activity, broadening the tax base and ultimately creating economic prosperity. The reality has fallen far short of the theory, however, as tax cuts have failed to boost investment in Taiwan or spur growth.

When CommonWealth reporters showed the list of companies earning more than NT$10 billion but paying effective tax rates lower than 1 percent to Taxation Administration director-general Wu Tzu-hsin, he turned to ask the agency's chief secretary, "Is it really that low?"

Wu was even more perplexed when he saw old-economy companies such as Far Eastern New Century and Asia Cement among the group with average effective tax rates below 1 percent, saying, "That doesn't seem possible. We will take a close look at this."

Part of the problem is that the Finance Ministry's internal study on companies' small tax burdens goes only as far as 2005. It found that the effective tax rates for the technology sector and old-economy companies were 5-7 percent and 13 percent, respectively. When asked about the extremely low rates paid by Far Eastern New Century, Asia Cement and others, the Finance Ministry responded: "We do not comment on specific companies."

"For a long time, the view inside the ministry has been that the amount companies underpay in taxes can be recouped when their big shareholders file personal income taxes. But it may be that it's hard to collect taxes at either end," says one official from the Tax Administration, which is under the Finance Ministry.

Lower Taxes Mean Greater Inequality

In his book The Price of Inequality, Nobel-winning economist Joseph E. Stiglitz argues that when governments relax their regulation of businesses and offer them tax breaks and other incentives, they inevitably sacrifice the rights of the general public and especially the average salaried worker and ultimately favor the wealthy.

For many years, successive finance ministers in Taiwan have trumpeted tax cuts as important administrative achievements. The only exceptions are Lin Chuan, who pushed through a 10 percent alternative minimum tax while heading the Finance Ministry from late 2002 to early 2006, and Chang Sheng-ford, who increased the alternative minimum tax to 12 percent last year.

Those measures have had some impact. Taiwan Semiconductor Manufacturing Co., the world's largest contract chip maker, used to pay an effective tax rate of just over 7 percent because of the many tax benefits it received for its high level of investment. At a recent investor conference, however, TSMC said it expected its effective tax rate this year would be over 13 percent.

But problems still abound, and KMT legislator and tax expert Tseng Chu-wei believes the biggest one is that those in power lack any sense of urgency to build a sound tax system.

"Go ask senior government officials what they see as the most serious problem today. Their answer may be the fourth nuclear power plant, pension reform or something else, but tax reform often ends up way down the list," an exasperated Tseng says.

If Taiwan's top decision-makers and financial officials cannot directly confront the low tax rates paid by wealthy individuals and corporations and the fact that Taiwan's government is in fact quite poor, it will be impossible for them to remedy the situation.

Taiwanese companies often defend their overseas tax avoidance schemes by saying they are "completely legal." But now that the Finance Ministry wants to finally get on the international bandwagon and pass amendments that will empower the government to tax offshore profits, the companies have banded together with lawmakers to block the legislation. No longer standing on the side of the law, they are determined to defend their interests, which will only impoverish Taiwan's government and people and widen the rich-poor divide.

British prime minister David Cameron is hoping to corral other countries at the G20 meeting in July into teaming up to crack down on multinational companies' tax avoidance schemes.

One of the questions for Taiwan's Legislature as its spring session winds down is whether it is willing to give legal backing to fighting the practice Cameron has spoken out against. If the lawmaking body passes critical amendments to the Income Tax Law on taxing overseas profits (Articles 43-3 and 43-4) and plugs the leak in corporate income taxes, legislators will finally have shown the resolve to stand up for the interests of the people they are supposed to represent.

As for the big domestic corporations that constantly criticize government officials for lacking an international perspective, they should support the internationalization of Taiwan's tax system. Only by shouldering their share of the country's tax burden will they be taking a real step toward fulfilling their corporate social responsibility.

Translated from the Chinese by Luke Sabatier

Views

Subscribe to CWE Newsletter (every Thursday)

Stay abreast of what's happening in Taiwan with our weekly digest.