Keeping 'Made In Taiwan' in Taiwan

Manufacturing Scrambles for a Future

Source:CW

Manufacturing is in transition, as people can no longer accept the loud, polluting factories of the past. CommonWealth Magazine takes a look at where the sector is headed in Taiwan.

Views

Manufacturing Scrambles for a Future

By Sara Wu, Jin ChenFrom CommonWealth Magazine (vol. 476 )

Taiwan's opening to independent travelers from China on July 1 was seen as a major step forward for the country's tourism sector and seemingly helped Taiwan edge closer to its dream: moving high-pollution industries and low-level jobs overseas and concentrating on the service sector and creative industries to bring economic prosperity and high-quality jobs.

The dream, however, is a far cry from reality. An economy based exclusively on services without manufacturing cannot be considered an ideal road for the country's future.

Over the past 10 years, advanced OECD countries whose economies have revolved around the financial and services sectors have all experienced the bitter taste of their manufacturers relocating abroad.

Reviving Manufacturing to Save America

In his book Fast Boat to China: Corporate Flight and the Consequences of Free Trade; Lessons from Shanghai, New York University professor Andrew Ross observed that offshore outsourcing is not just about individual factories. It's about uprooting an entire industrial chain, resulting in high unemployment, community degradation and a diminishing tax base.

The first to suffer from the trend was the United States.

In 2010, manufacturing accounted for about 22 percent of the country's GDP, setting a new historical low. Over the past 10 years, the U.S. has had 40,000 factories move abroad, resulting in the loss of 5.5 million jobs. From furniture and cars to mobile phones, entire American industries have abandoned manufacturing.

The financial crisis in late 2008 and 2009 forced the United States to examine itself more critically, realizing that when the financial services sector is the engine of a country's economy and trouble hits, the first indicator to be adversely affected is unemployment, which has reached a plateau of 9 percent. The New York Times warned President Barack Obama that no U.S. president in the history of the country has been re-elected when the unemployment rate is higher than 7.2 percent, and Obama may have been listening.

On June 24, the U.S. president announced he was forming an "advanced manufacturing partnership," to be headed by Dow Chemical Co. chairman and CEO Andrew Liveris and Massachusetts Institute of Technology president Susan Hockfield.

Obama clearly hopes to use the initiative to spark a renaissance of American manufacturing and ensure that "tomorrow's breakthroughs are American breakthroughs. We're teaming up… to create the kind of innovation infrastructure necessary to get ideas from the drawing board to the manufacturing floor to the market more rapidly – all of which will make our businesses more competitive and create new, high-quality manufacturing jobs."

Liveris is particularly concerned about the United States losing its manufacturing edge. He cited the example of the e-book reader Kindle, conceived through American innovation and ideas but built by a Taiwanese company, to warn America that the lack of manufacturing is tantamount to giving up control of lucrative emerging industries.

Taiwanese Company Milks American Cow

In 2007, in a mystery laboratory in Silicon Valley called Lab 126, an engineer and a designer succeeded in developing a new product – Kindle – that would change the way the world reads books and become the first item Amazon would try to market under its own brand name.

Kindle created a stir not only because it serves as a portable library, but also because it marked the launch of a new-generation electric ink technology. Only one company in all of America was capable of manufacturing this type of technology – E Ink Corporation.

E Ink was not capable, however, of manufacturing the Kindle screen in-house and had to rely on the LCD display production technology of Hsinchu-based Prime View International Co. (later renamed E Ink Holdings Inc.) to bring the product to market.

"The strength of Taiwan's manufacturing is 'from lab to fab,' its ability to take a sample made in a laboratory and turn it into a mass-produced product," says E Ink Holdings chairman Scott Liu.

In 2009, Prime View acquired E Ink Corp. for NT$7 billion, and then changed its own name to E Ink Holdings, becoming the only company in the world capable of producing electronic paper and seizing a virtual monopoly on e-reader components.

According to Digitimes analyst James Wang, 23.5 million e-readers will be sold this year, and E Ink Holdings will have over 90 percent of that market. Regardless of whether the e-reader is Amazon's Kindle, Nokia's Nook, Japan's Sony or China's Hanwang, they all use E Ink's electronic paper. Because of its virtual monopoly in the market, the company has a gross margin exceeding 30 percent, higher than that of the vast majority of high-tech companies.

Yet while Taiwan's manufacturing prowess was once praised effusively by innovation guru Clayton Christensen, warnings of trouble on the horizon have gradually begun to surface.

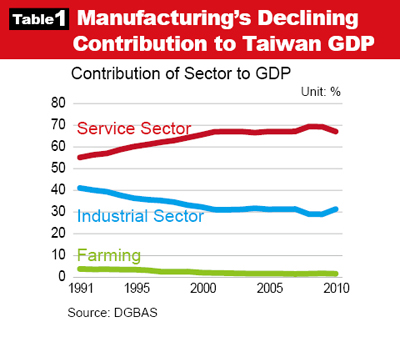

As in America, manufacturing's contribution to Taiwan's GDP has been on the decline, falling from 40 percent in 1990 to just below 30 percent in 2009 before rebounding slightly to 31 percent in 2010. (Table 1)

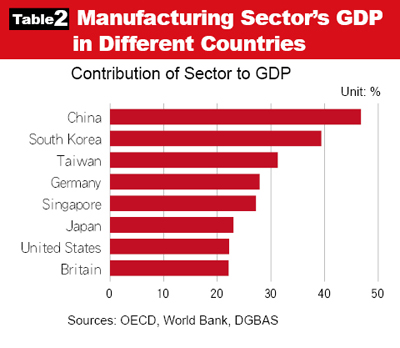

When benchmarked against advanced economies, these numbers provide little comfort. Manufacturing accounts for 28 percent of GDP in Germany and 27 percent in Singapore. If Taiwan's manufacturing sector continues its decline into the future to levels seen in the U.S., Britain and Japan, the country's GDP structure runs the risk of lacking diversity. (Table 2)

Advanced Manufacturing = Good Jobs

Another risk of an economy increasingly dependent on services is employment.

The number of Taiwanese employed in manufacturing has fallen from 42 percent in 1990 to 36 percent in 2010, and economists believe the trend is one of the factors behind Taiwan's persistently low wage levels. Chang Chien-Yi, the deputy director of the Taiwan Institute of Economic Research's Division II, says Taiwan's service sector accounts for 70 percent of the country's GDP and employs nearly 60 percent of its workforce, but its contribution to economic growth remains limited, and it only rarely generates salary increases. Of Taiwan's 10.82 percent growth in 2010, 70 percent came from the manufacturing sector.

According to figures from the Directorate-General of Budget, Accounting and Statistics, the average salary in Taiwan's top 10 manufacturing sectors was NT$61,000, far above the NT$43,000 average in the country's top 10 service sectors. Even within the service sector, the best paying jobs can be found in businesses providing support to manufacturers rather than the wholesaling and retailing sectors, which employ the most people.

Manufacturing is also unrivaled in its ripple effect on job creation. According to the U.S. Bureau of Economic Analysis, manufacturing has the greatest multiplier effect on the economy of any major sector, supporting US$1.40 in output from other sectors of the economy for every dollar in final sales of manufactured products.

For the sake of economic development and job creation, countries round the globe have no choice but to join in the fierce contest to attract manufacturing. It's not just the United States. Even China, with its reputation as the world's factory, is locked in the battle to snatch, and hold onto, manufacturing contracts.

Governors of provinces from around China have relentlessly solicited investment in production facilities from Taiwanese companies, but persistently rising wages have recently emerged as the biggest obstacle in China's pursuit of an even bigger share of the manufacturing pie.

A report issued in May by the U.S.-based Boston Consulting Group (BCG) said that with wages in China rising by 17 percent a year and the continued appreciation of China's currency, combined with the relatively higher productivity of American workers, net labor costs for manufacturing in China and the U.S. are expected to converge by around 2015.

"As a result of the changing economics, you're going to see a lot more products 'Made in the USA' in the next five years," said Harold L. Sirkin, a BCG senior partner. The report pointed to states with flexible work rules and government incentives, such as Mississippi, South Carolina and Alabama, as being increasingly competitive as low-cost manufacturing bases for supplying the U.S. market and potentially capable of serving as a substitute for China.

The BCG report caused an uproar in China, with Chinese media giving prominent coverage to the unprecedented challenges faced by the country's manufacturing sector that could affect its very survival.

What Kind of Manufacturing Does Taiwan Want?

This year, Taiwan bravely rejected the proposed Kuokuang petrochemical complex that was to be located in a wetland in Jhanghua County. But if Taiwan's people have reached a consensus that they do not want high energy consumption businesses, then what kind of manufacturing sector does the country want to preserve?

"If an effort isn't made to upgrade the manufacturing sector, there will certainly be a hollowing out of manufacturing businesses," says a concerned Tyzz-Jiun Duh, the director general of Taiwan's Industrial Development Bureau.

The bureau, Duh said, has abandoned traditional concepts focusing solely on investing resources and expanding capacity to upgrade factories' production capabilities. Instead, the bureau has already drafted an industrial development strategy that would increase the rate of added value, raise the ratio of intangible assets to total fixed capital to 15 percent, and increase the share of green energy businesses to 30 percent of the total output of the manufacturing sector, all by 2020.

If the conventional concept of production capacity is no longer sufficient to measure the value of a business, then what are the new standards?

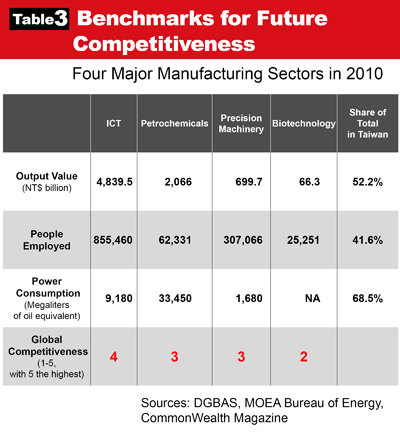

CommonWealth Magazine has identified four indicators – output value, job creation, energy consumption, and global competitiveness – to re-evaluate the strengths and weaknesses of four major manufacturing sectors: petrochemicals, precision machinery, information and communications technology (ICT), and biotechnology. (Table 3)

As the table shows, Taiwan's petrochemical industry is high-value, yet it employs relatively few workers and consumes considerable energy, raising questions over its sustainability. Overall, it earns a medium grade in terms of global competitiveness.

Another sector with mid-range competitiveness is precision machinery, with reasonably high output value and high job creation, and very low energy consumption.

The true star, however, is ICT, with very high output value, high employment, moderate energy consumption, and robust global competitiveness. ICT clearly clocks in as Taiwan's most important manufacturing sector.

Currently, Taiwanese biotechnology can only boast low output valuae and job creation, but it is notable for its high growth potential.

Can the island's manufacturers generate high value and claim a leading position in the global market, while burning less fuel in the process? The answer has implications not only for business development, but also for the livelihoods of tomorrow's Taiwanese. With the future of the country's manufacturing sector currently being charted and its role debated, nothing less than the vitality of Taiwan's economy and its ability to generate quality jobs are at stake.

Translated from the Chinese by Luke Sabatier

Views

Subscribe to CWE Newsletter (every Thursday)

Stay abreast of what's happening in Taiwan with our weekly digest.